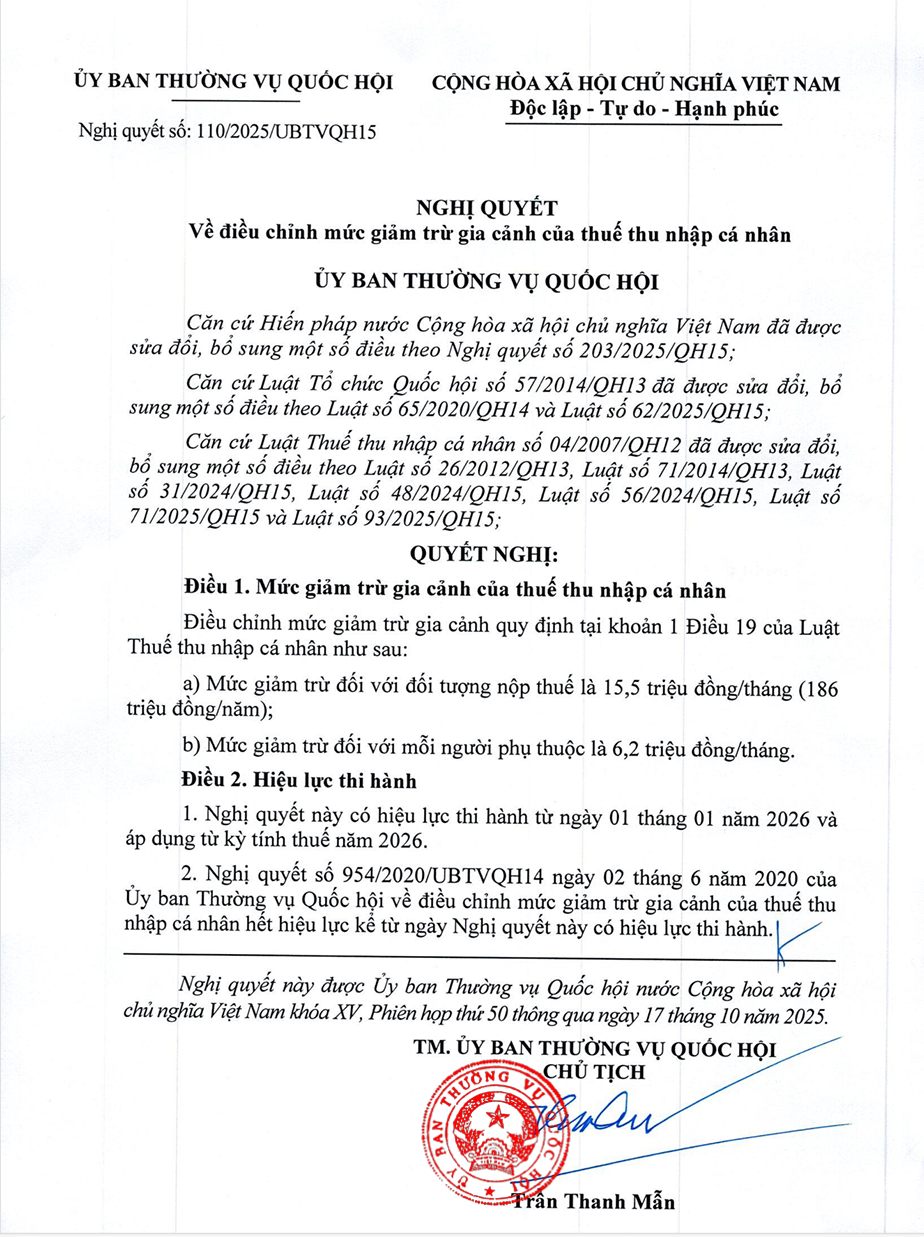

Accordingly, Resolution 110/2025/UBTVQH15 adjusts the family deduction level prescribed in Clause 1, Article 19 of the 2007 Law on Personal Income Tax as follows:

– The deduction for taxpayers is 15.5 million VND/month (186 million VND/year);

– The deduction for each dependent is 6.2 million VND/month.

Currently, Resolution 954/2020/UBTVQH14 stipulates the family deduction level as follows:

– The deduction for taxpayers is 11 million VND/month (132 million VND/year);

– The deduction for each dependent is 4.4 million VND/month.

Thus, from the 2026 tax period, the family deduction for taxpayers will be officially increased to 15.5 million VND/month and the family deduction for each dependent will be increased to 6.2 million VND/month.

Note:

– Family deduction is the amount deducted from taxable income before calculating tax on income from salaries and wages of taxpayers who are resident individuals.

– Determining the family deduction level for dependents is implemented according to the principle that each dependent is only deducted once for a taxpayer.

– Dependents are people that the taxpayer is responsible for supporting, including:

+ Minors; disabled children, unable to work;

+ Individuals with no income or with income not exceeding the prescribed level, including adult children studying at university, college, vocational high school or vocational training; spouses who are unable to work; parents who are past working age or unable to work; other people without support that the taxpayer must directly support.

Resolution 110/2025/UBTVQH15 takes effect from January 1, 2026 and applies from the 2026 tax period.

Resolution 954/2020/UBTVQH14 of the National Assembly Standing Committee on adjusting the family deduction level of personal income tax ceases to be effective from the effective date of Resolution 110/2025/UBTVQH15.